Commodity markets are currently, all about the weather, the funds and currency. US soil conditions are a bit like the curate’s egg, there are some rotten bits as well as parts that are excellent. S Wisconsin and N Illinois are suffering from floods, but almost everywhere else is a bit dry. The current situation in localised areas of Montana, North Dakota and South Dakota, where most of

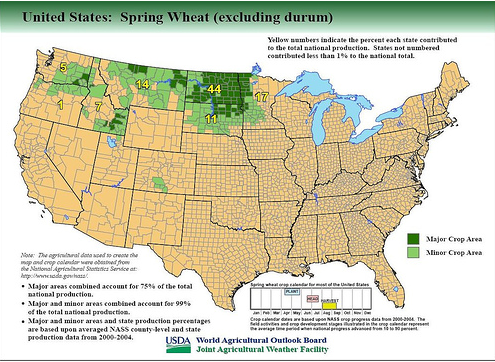

the milling wheat grown (see US map), is dire, as they are suffering from the worst drought in three decades with very little to harvest and the lack of water and forage forcing some farmers to sell their cattle. As of July 23rd Spring wheat crop ratings were put at 33% very poor, 22% poor, 32% fair, 10% good and 3% excellent. The province of Saskatchewan (SK) lies across the northern border of Montana and N Dakota, where half of Canada’s wheat crop is grown; it is

also suffering from lack of recent rainfall (see SK map). As of July 24th 58% of its spring wheat crop was good/excellent, so not as bad a situation as its southern neighbours. The weather maps show more rain and thunder storms moving across the northern Plains and upper Midwest this week which are viewed as being beneficial to crops; Iowa is predicted to receive an inch of rain, with generally cooler weather across the Corn Belt. The Wheat Quality Council tour of spring wheat fields has been completed, and the 2017 US hard red spring wheat crop is expected to yield 38.1b/a (45.7 b/a last year, 5-year average 46.8 b/a).

In Europe the combines are dodging about trying to avoid the rain clouds. In France the soft wheat harvest is 85% complete (of an expected 37mt), and the durum wheat harvest is all in the barn. There is growing concern about the state of German milling wheat if the rain continues. It seems obvious that US exports of milling wheat will be impaired this year, if Germany suffers a similar fate, then we envisage that there might be a high milling wheat premium in the UK. We had our first deliveries of new crop wheat this week, the earliest cut for a number of years, and the quality on initial inspection was excellent (the analysis will follow in due course). The IGC estimates for the global wheat crop for 2017/18 have been trimmed by 3mt to 732mt due to the US (46.7mt previously 48.6mt), Australia (22.8mt previously 24.8mt) and the EU (148.1mt previously 149.4mt). As previously reported, Russia is hoping to hit last year’s record (72.5mt) and the IGC increased its estimate from 68mt to 71mt.

US soya condition ratings are falling, and were reduced by 4% down to 57% good/excellent from last week. (71% last year). About 70% of the soya is flowering, so weather conditions will be critical as pollination takes place over the next few weeks; as the Americans say, ‘soya is made in August’. The USDA’s July estimate was that soya yields will be 48b/a though OilWorld is suggesting 46.8 b/a and Strategie Grains 47 b/a. Although US soya production is expected to be slightly lower at this stage, there is plenty of soya in South America as Argentina sold over 1.2mt last week bringing their total sales to 29.4mt (31mt last year), which represents about 50% of their production. Brazilian farmers are reluctant sellers, partly due to currency, and have only sold about 75% of their crop to date compared to 88% at this time last year. Globally, the IGC believe that 2017/18 soya production will be 345mt, the second biggest on record. GM soya is about £290 delivered to the mill.

Despite parts of Wisconsin suffering from flooding, more than 100 competitors from around the world assembled to hold the World Lumberjack Championships last weekend.

Which reminds me of Month Python’s 1969 sketch. 'I'm a lumberjack and I’m okay'

Regards Paul Poornan and Martin Humphrey